Markets

Markets

Apollo Tyres faces twin speedbumps of rising costs, weak demand

Summary

- The company does have a cushion, though, with high-margin segments growing their share and debt falling.

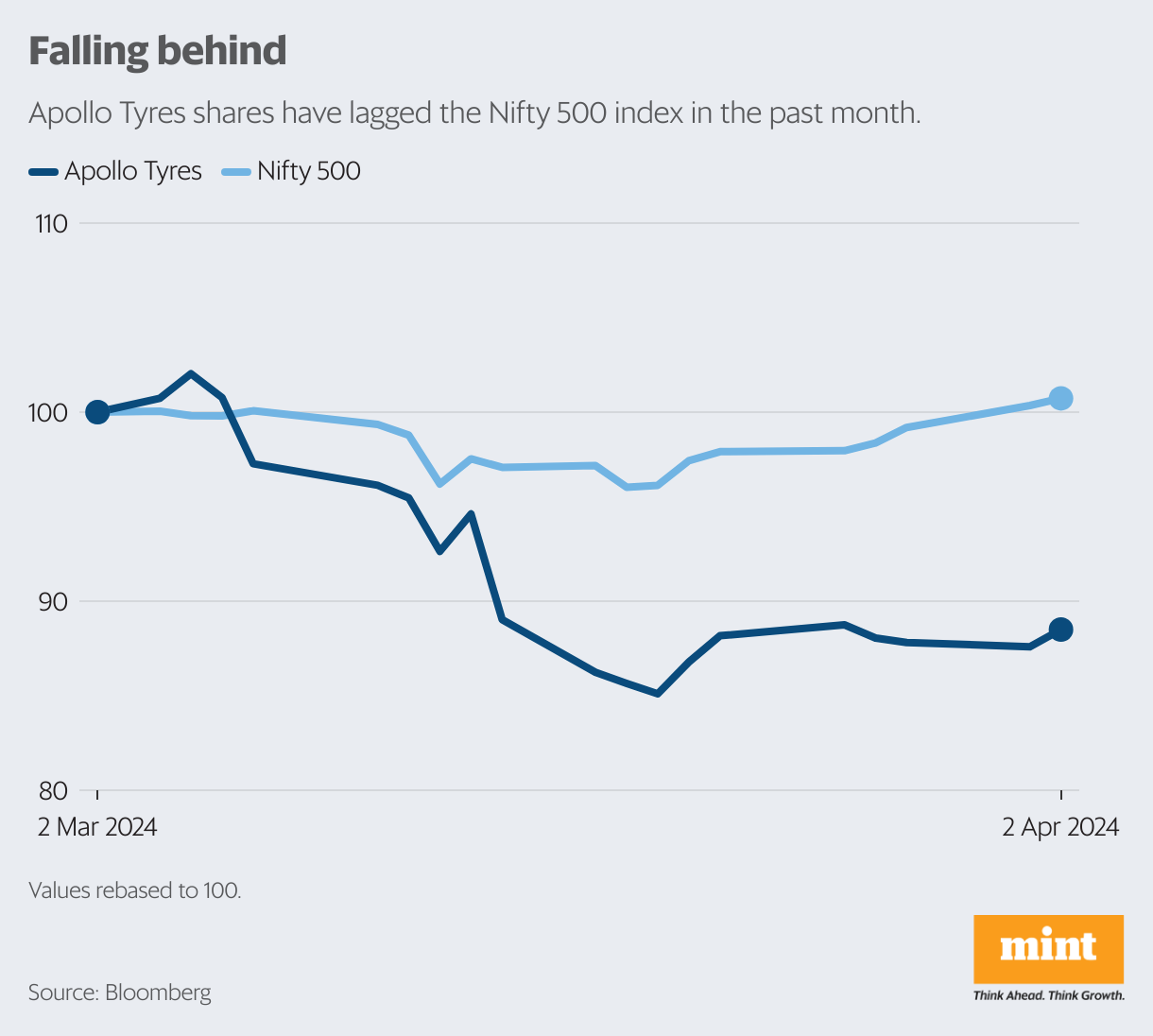

Apollo Tyres Ltd stock has underperformed the market over the past month. Investors have understandably turned cautious amid the recent spike in prices of rubber, and demand is expected to be weak in the near term. But the company does have a cushion, with high-margin segments growing their share and debt falling.

The company’s financials have been highly erratic over the past five years owing to the pandemic and commodity-price fluctuations, which have a strong influence on profitability.

For instance, in FY21, while consolidated revenue growth stood at 6% year-on-year, Ebitda growth came in at 44%. Ebitda is earnings before interest, tax, depreciation, and amortization. However, in FY22, a steep rise in raw-material costs caused Ebitda to drop by 8% at a time when revenues grew by 20%. As a result, Ebitda margin contracted to 12% in FY22 from about 16% in the previous year.

With the softening of raw-material prices, Apollo’s performance improved in FY23 and continued to do so in 9MFY24, with Ebitda rising by 29% and 48% and revenue growth by 17% and 4%, respectively.Apollo’s revenue in 9MFY24 was ₹19,119 crore and its Ebitda margin was almost 18%. Note that the margin expansion was due not just to softening raw-material prices but the changing customer mix as well. More importantly, the Indian market is also moving towards ‘premiumization’, with increasing sales of SUVs and higher radialization in truck and bus tyres. Radialization refers to shifting from traditional tyres that use nylon threads to ones that use steel wires.

The four-year moving average of the share of SUVs in passenger-vehicle sales has increased from 22% in FY20 to an estimated 43% in FY24, and is projected to touch 53% by FY26, according to an Emkay Global Financial Services report. Similarly, the level of radialization is estimated to have risen from 49% in FY20 to 63% in FY24.

It also helps that Apollo’s debt is falling. As of the end of December, consolidated net debt dropped to ₹3,000 crore from ₹3,830 crore at end-September. The net-debt-to-Ebitda ratio fell to 0.7 times by endDecember from 1.4 at end-FY23.

Apollo’s shares trade at 14.3 times its estimated FY25 earnings, according to Bloomberg. Sure, valuations appear undemanding, but near-term triggers seem limited amid anticipated margin pressure. Against this backdrop, investors will watch the company’s pricing actions closely.

The company's capital expenditure (capex) guidance for FY24 is around ₹1,100 crore and is expected to be used for de-bottlenecking, digitization and maintenance activities. Latest management commentary suggests that capex intensity is likely to remain low in the medium term, which bodes well for return ratios and the health of the balance sheet.