Markets

Markets

Is Axis Bank's share price fall a knee-jerk reaction?

")

Summary

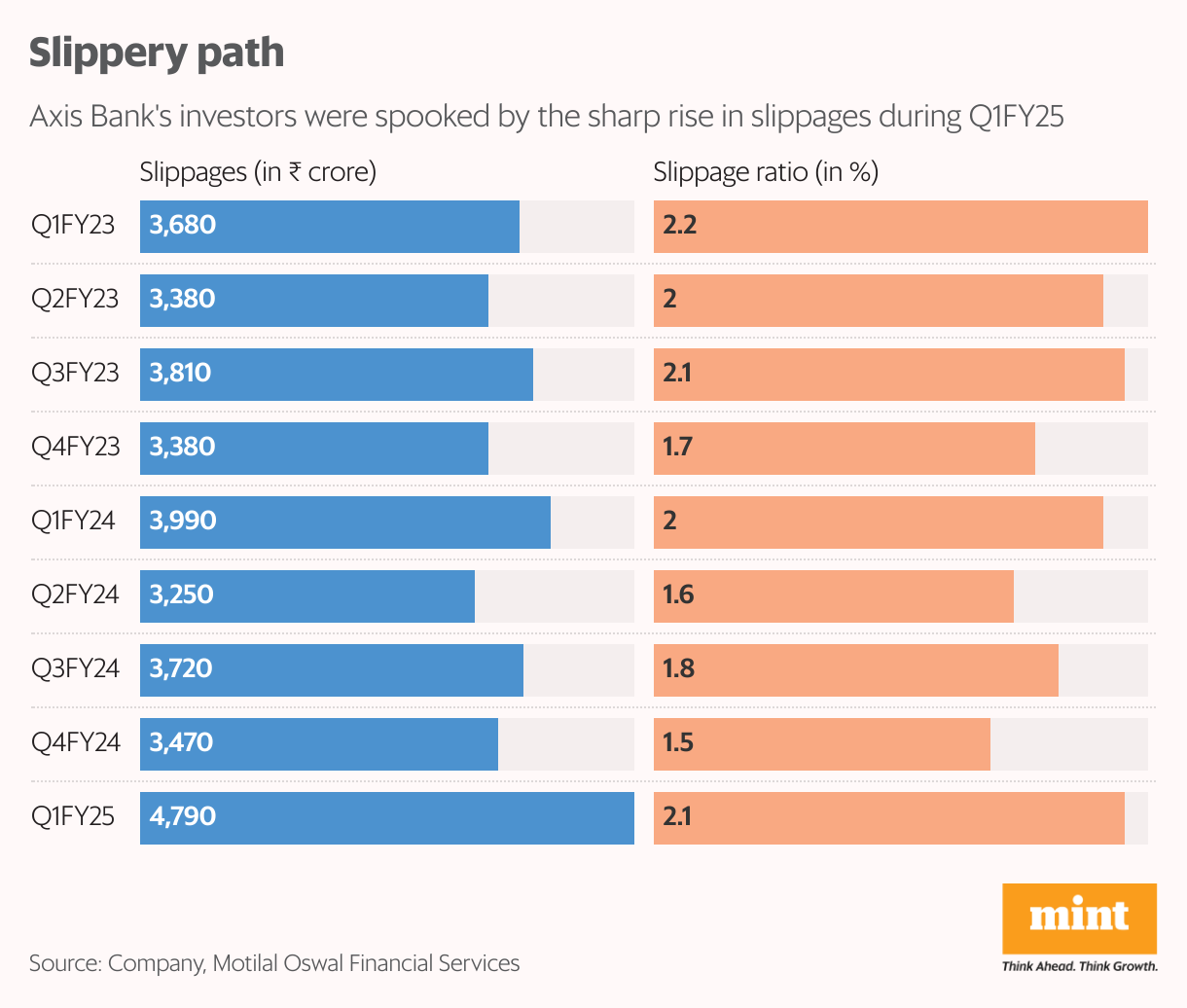

- Axis Bank investors seem concerned about the surge in the credit cost

- Personal loans and credit card loans grew much faster than the overall loan book growth

Axis Bank was the top loser among Nifty 50 stocks on Thursday, declining by about 6%. Despite a satisfactory show on key parameters in the June quarter (Q1FY25), investors seem more concerned about the surge in the credit cost. There is no clarity on whether the increase in credit cost is a one-off or beginning of a trend.

The management clarified during the earnings call that the annualized net credit cost of 0.97% based on Q1FY25 may not be the correct indicator for FY25. It reckons that the bulk of the higher credit cost last quarter was on account of seasonality and lower recoveries.

“We would have to wait and watch to test the thesis that it could be a less painful period than what the bank has experienced previously," said analysts from Kotak Institutional Equities.

Against this backdrop, Thursday’s fall in the share price appears to be more about unfair expectation of investors that the credit cost in future would remain at the trough level of FY24. Note that credit cost or provision for NPAs and slippages or fresh gross NPAs generally move in tandem. RBI’s Financial Stability Report says FY24 was the best year in the last 12 years with gross NPA of banks hitting a low of 2.8%.

Axis Bank’s gross slippage ratio, simply put, fresh addition to NPAs, has risen to about 2% from 1.4% in the preceding quarter with a significant chunk of the slippages coming from retail portfolio. The retail portfolio accounts for 60% of the total loan portfolio. Notably, almost 30% of the retail portfolio is unsecured, implying 18% (30% of 60%) as high-risk portfolio. That high-risk portfolio is growing faster than the secured portfolio.

Also Read: Axis Bank reiterates system deposit, credit growth to converge over FY25

Personal loans and credit card loans, both part of unsecured loans, grew year-on-year by 29% and 22%, respectively, much faster than the 14% overall loan book growth. RBI has been cautioning about a surge in unsecured household debt or consumption loans even though India's household debt is among the lowest in the world. It has risen to around 40% of GDP in FY24 from 38% a year ago.

Barring the slippage and credit cost part, Axis Bank’s net interest income grew by 12% year-on-year in Q1FY25 even though the pressure on CASA ratio is evident. Strong operating income coupled with a lower rise in operating costs helped in a robust pre-provisioning operating profit growth of 15%. However, the good part ends here. Loan loss provisions doubled year-on-year to ₹2,298 crore. Consequently, pre-tax profit growth was 4%.

Also Read: Axis Bank vs ICICI Bank: Which is the best Indian banking stock?