Industry

Industry

If deposits are stuttering, how will banks manage the credit boom?

")

Summary

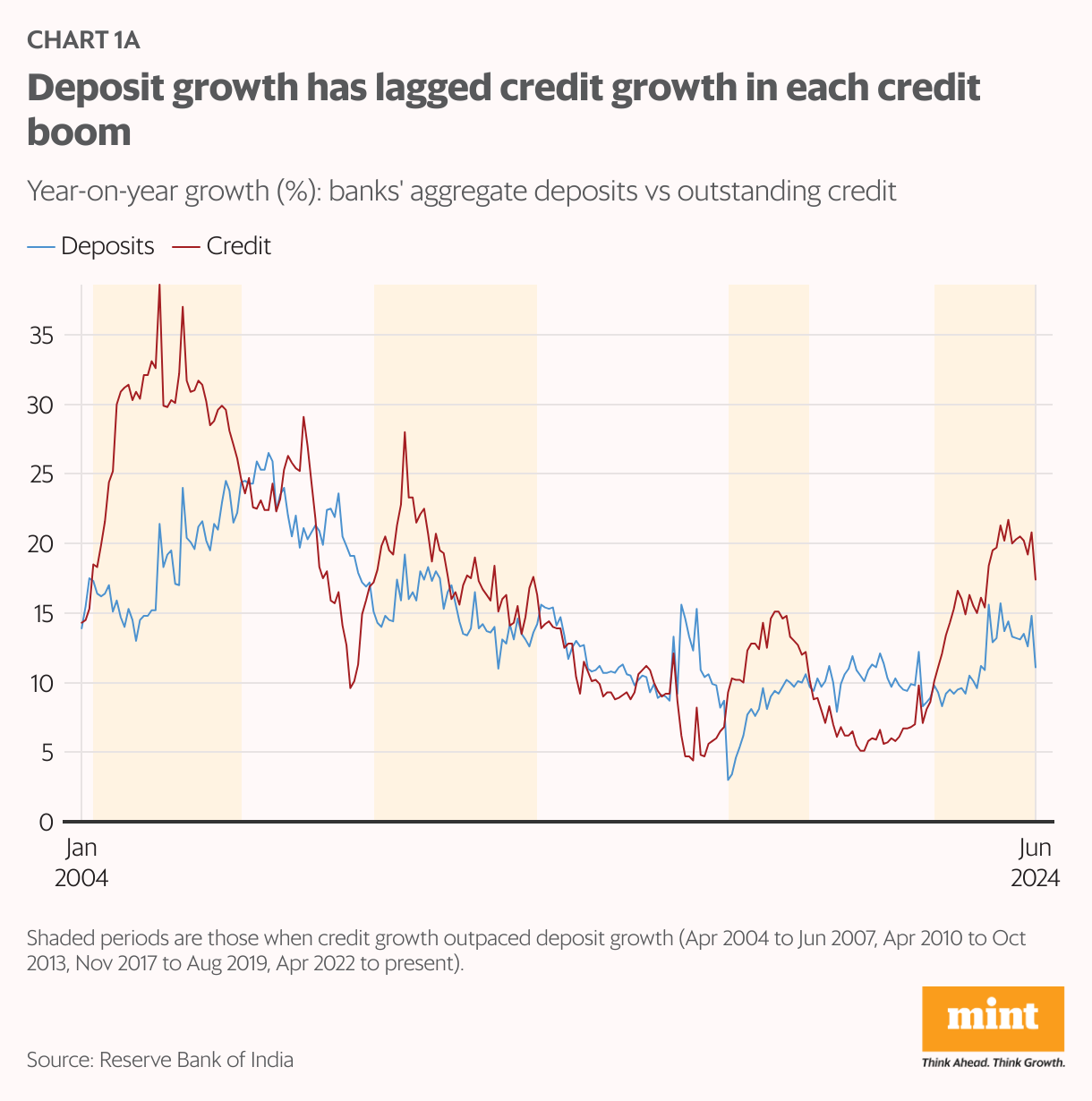

Amid the post-pandemic credit frenzy, banks are having to fund loans through higher deposit rates and other high-cost sources. It’s come to haunt their interest margins. The path ahead needs to be handled delicately.Bank credit has been on a roll for a while now. The post-pandemic pickup in credit that began in April 2022 has gained momentum, clocking a brisk 19-20% year-on-year growth over the past 10 months. However, deposits have lagged, growing at a modest rate of 12-13%.

This disparity presents a challenge for banks, as they need deposit growth to be robust enough to fund the increasing volume of loans they are extending. This mismatch between credit and deposit growth, however, is not unprecedented, having been a feature of previous lending booms since 2004. In fact, the current gap is less severe than during the 2004-2007 cycle.

Read this | Indian banks are battling the worst deposit crunch in 20 years

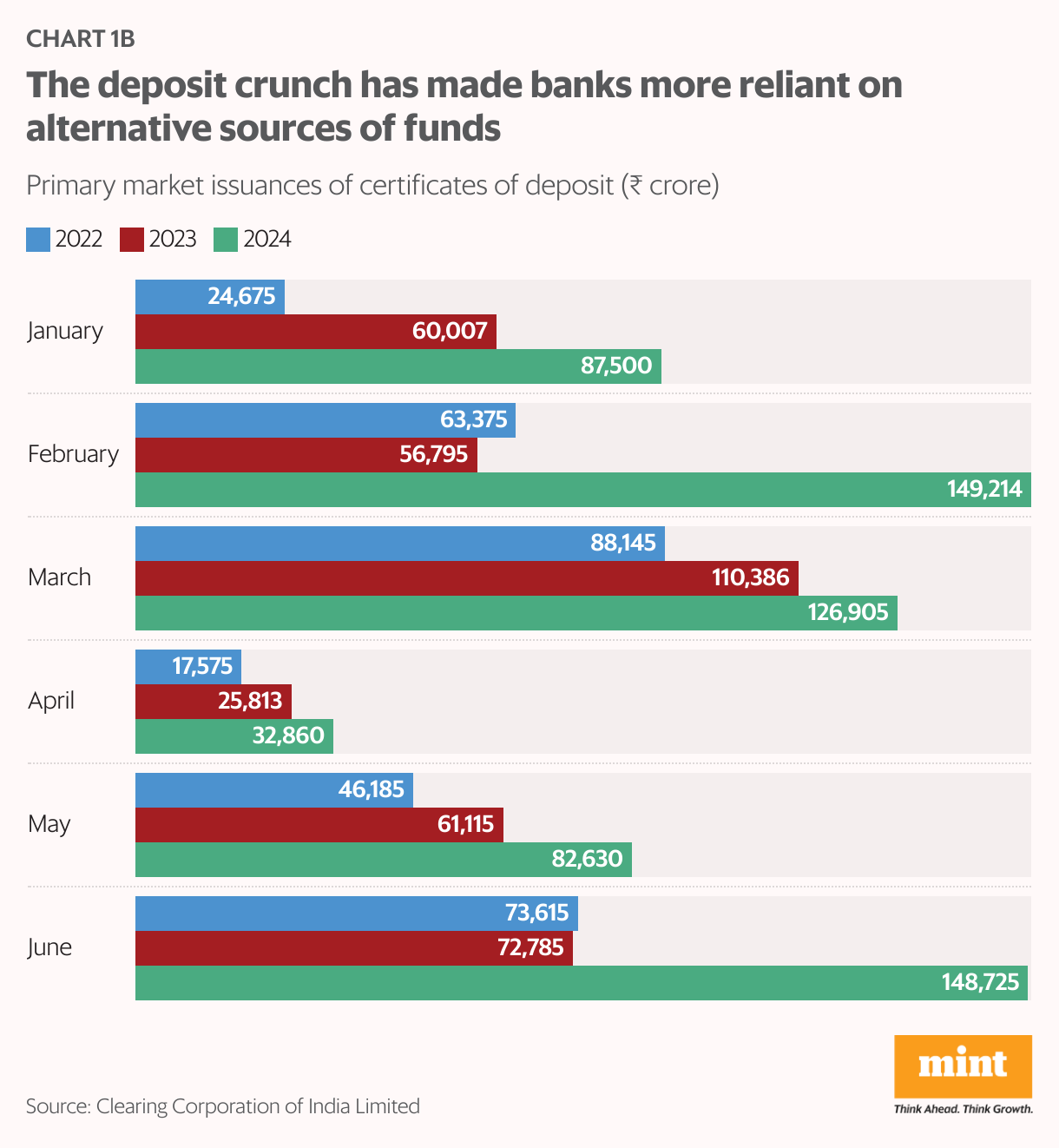

Two key features characterize the present cycle: first, banks are increasingly turning to alternative, non-deposit sources of funding. The issuance of certificates of deposits (CDs, wholesale deposits in a way) has surged, with banks raising ₹2.64 trillion through CDs in the June quarter alone, accounting for about 30% of new deposits. This dependence on CDs, while growing, remains below levels seen in previous credit booms. For instance, between November 2010 and March 2011, facing a similar credit-deposit gap, banks raised ₹5 trillion through CDs, which was double the amount of deposits added during that period.

Second, the current deposit growth rate, although slower, is closer to its long-term trend, indicating a more sustainable trajectory. This contrasts sharply with 2007, when deposit growth exceeded 25% for several months, and the 2017-2019 period, when it dipped below 10%.

Deposit franchise

The 'deposit franchise' of banks—their ability to attract and retain low-cost deposits—is extremely valuable. This value is derived from the type and ownership of the deposits they attract, as well as their capacity to maintain these deposits even as interest rates fluctuate.

The greater the share of low-cost current and savings accounts (CASA), the greater the value of a bank’s deposit franchise. This is particularly crucial for deposits held by individuals or small businesses, since sophisticated corporate depositors can shift funds swiftly, a truth that was brought home last year when rapid withdrawals by Silicon Valley Bank’s high net-worth customers precipitated its collapse.

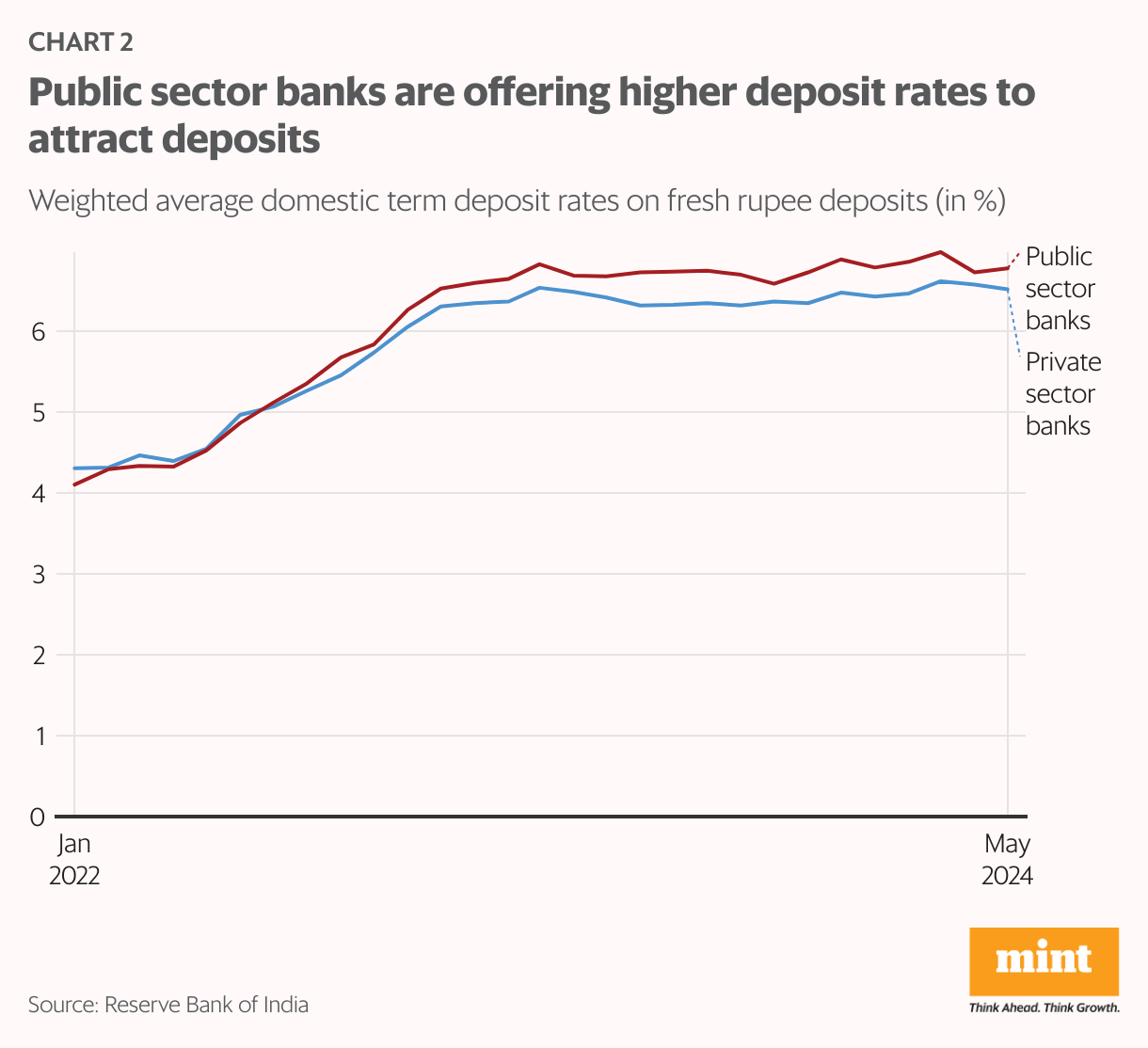

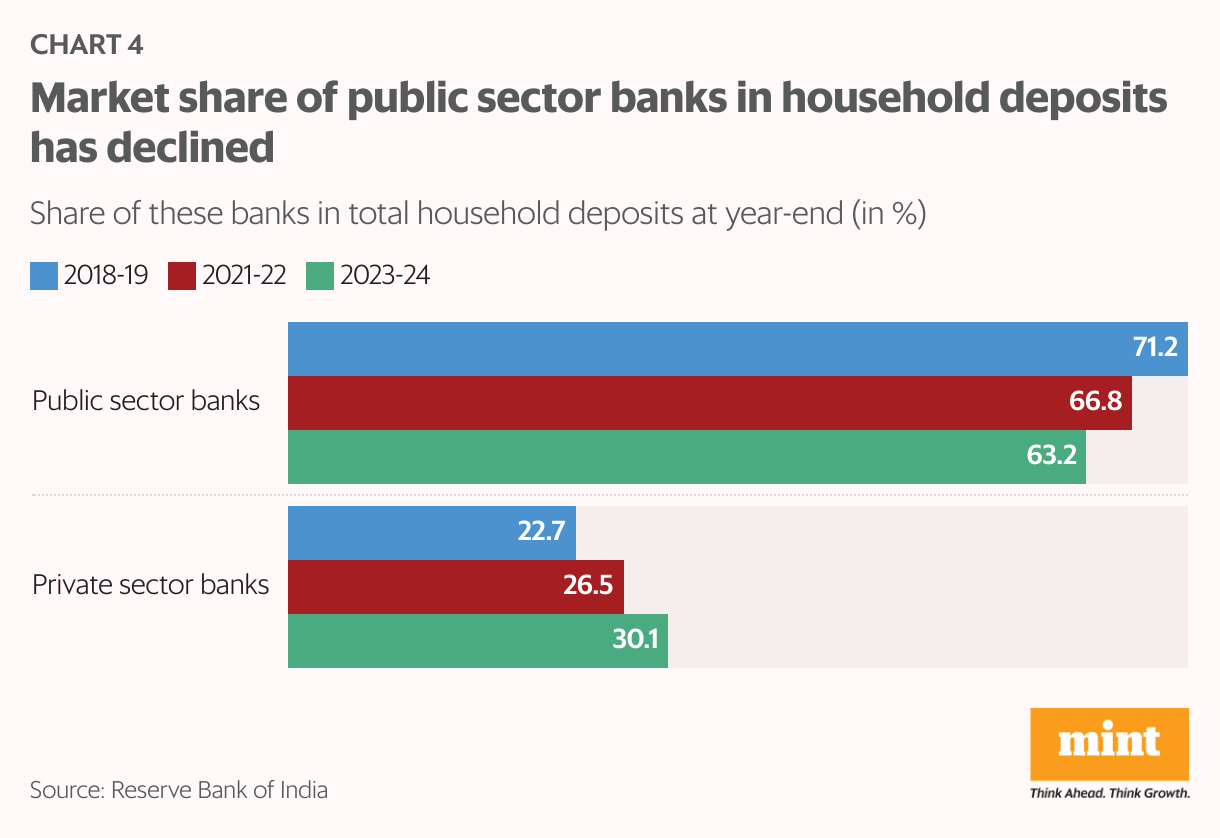

In response to the current lag in deposit growth, public sector banks are offering higher rates on fresh term deposits than private sector banks. This can strengthen their ‘deposit franchise’ by increasing the share of household deposits in their portfolio, while also leveraging their reputation as government-backed institutions designed to serve the common people.

Interest margins

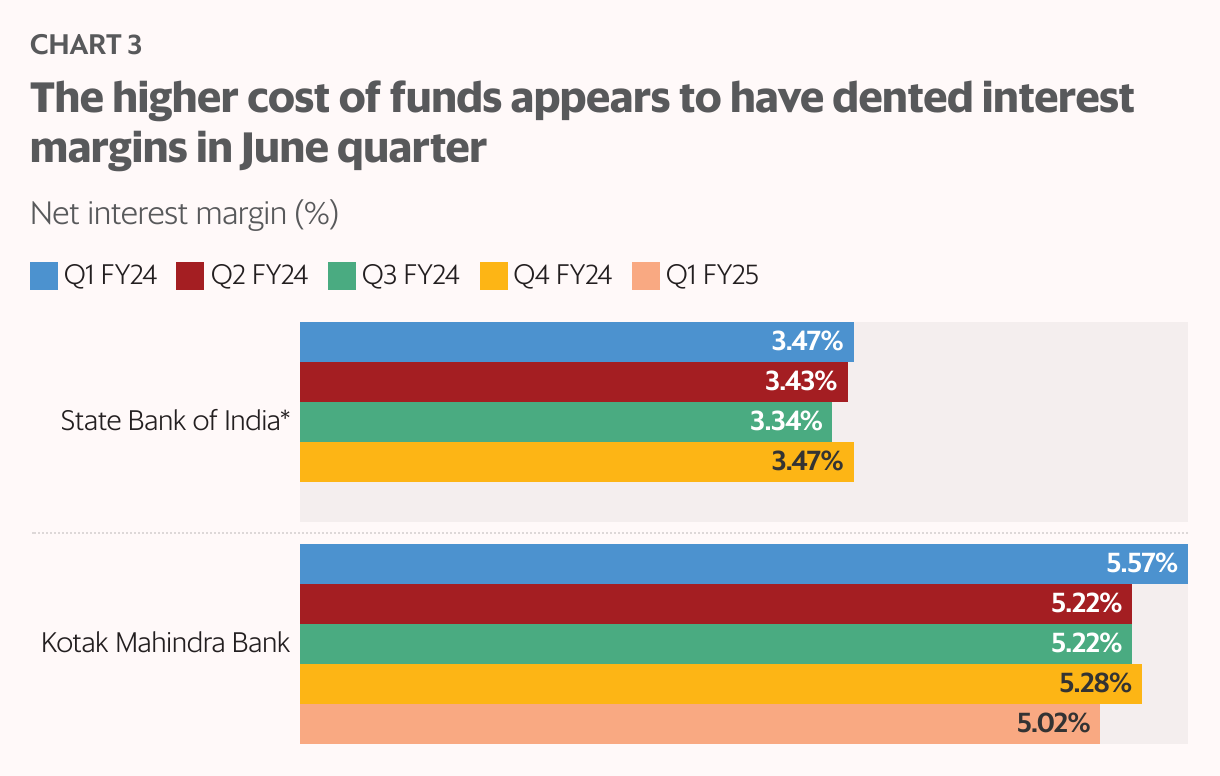

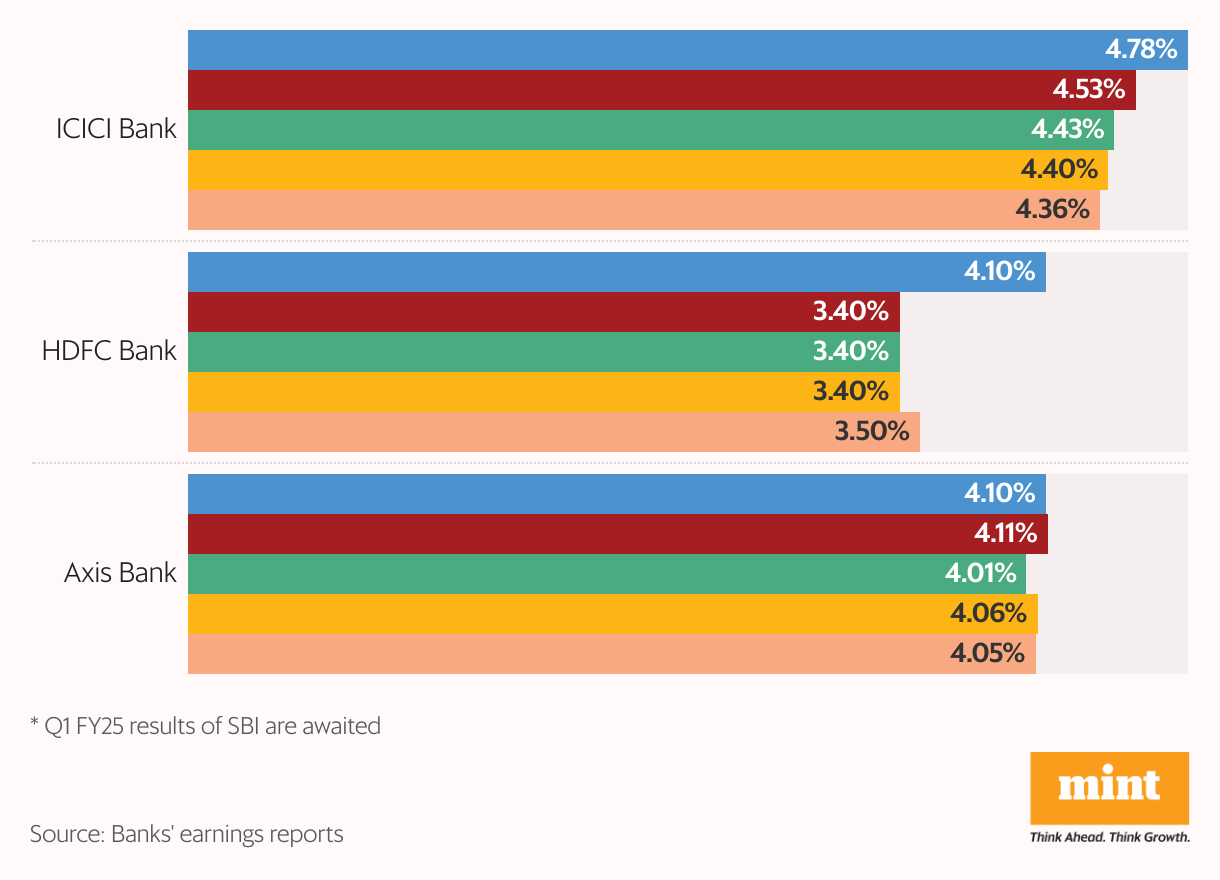

For banks, procuring funds to lend away has become costlier as they have had to raise deposit rates and depend more on higher-cost sources. At the same time, interest earnings have also risen because they have raised lending rates, too. The final impact on profitability is still playing out, but three of the top five banks saw net interest margin (NIM) drop in the June quarter.

When monetary policy is tight and demand for credit is strong, as it is now, banks quickly pass on rate hikes to the credit side; they raise deposit rates only if deposit growth is lagging. As a result, NIM usually increases in the early part of a credit boom, and either plateaus or decreases towards the end. But that trajectory is not a given: Much will depend on the policy stance and market liquidity as well as bank-specific credit and deposit dynamics, and banks will keep an eye on those factors.

Way ahead

Although common for a bullish credit cycle, a credit–deposit growth imbalance is concerning. As the Reserve Bank of India governor recently pointed out, a severe imbalance poses “structural liquidity issues" for the system. It also forces banks to rely more on high-cost borrowings, which erodes margins. Not surprisingly, banks have increased lending rates twice in the last two months.

Lessons from past credit booms provide valuable insights but are insufficient to address the current deposit crunch. Demographic changes, technological advancements, and income growth have led to a structural shift in savings and investment behaviours.

Also read | The anatomy of a post-crisis monetary policy, explained

Banks must manage their deposit franchises more strategically rather than assuming they will maintain their share as before. Offering differentiated products and building a strong digital presence will be essential for attracting customers. Public sector banks, in particular, need to focus on regaining their core customer base, as they have lost market share in household deposits to private banks.

The author is an independent writer on economics and finance.