Markets

Markets

Colgate’s valuations get richer after top class performance in Q1

Summary

- Colgate’s efforts at category development and product innovations seem to be paying off

- With the impact of earlier price hikes fading, revenue growth may moderate ahead

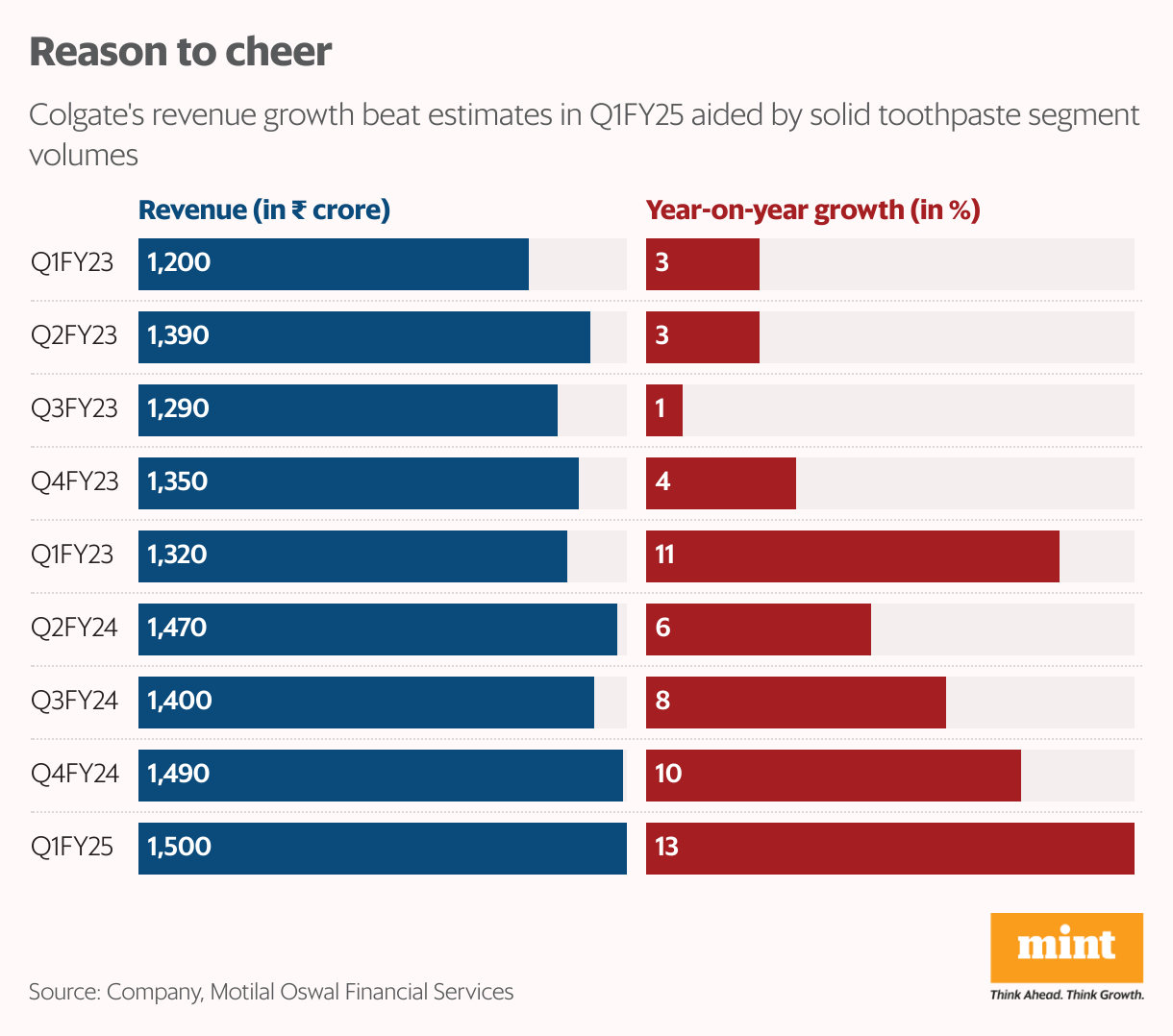

Heading into the June quarter (Q1FY25) results, expectations were quite restrained for Colgate-Palmolive (India) Ltd. For the company’s toothpaste business, most analysts had projected last quarter’s volume growth at 2-3%. But Colgate beat those estimates significantly and said the toothpaste segment clocked a high-single digit volume growth. Investors cheered, taking the stock up by over 5% on Tuesday, also touching a new 52-week high of ₹3424.95 apiece.

Colgate’s total operating revenue in Q1 rose by 13% year-on-year to ₹1,497 crore. In comparison, Hindustan Unilever Ltd’s oral care segment saw mid-single-digit value growth led by pricing. Colgate said demand pickup in the rural markets outpaced the growth in urban markets for the second quarter in a row. This, along with good all-round performance in toothpaste, toothbrush and personal care, meant Colgate’s domestic revenue was up 12.8% last quarter. The toothbrush portfolio saw strong double-digit revenue growth.

What’s even better is that Q1’s Ebitda growth was relatively faster at 21.5% year-on-year to ₹508 crore aided by margin expansion of 238 basis points (bps) to 34%. This was despite staff costs rising by 17%. Profitability was helped by a slower pace of increase in raw material costs and advertising expenses. The strong show across parameters has pushed analysts to raise their earnings estimates for this year and the next.

Colgate’s efforts at category development and product innovations seem to be paying off. In FY24, Colgate’s Ebitda margin had climbed 386 bps year-on-year to 33.5%, leading to 23% growth in Ebitda. But the path ahead is challenging. Margin expansion could be limited.

Read more: Equities mood check: Peaky markets, crawling earnings

“While premiumization trend will continue and aid margin improvement, we expect its contribution to be limited. We believe if further price hikes are effected, higher than peers, it could lead to market share loss," says Mihir P. Shah, analyst at Nomura Financial Advisory and Securities (India). Thus, Colgate may not choose to use price hikes as a margin driver like it did in FY24, according to Shah.

With the impact of earlier price hikes fading, revenue growth may moderate ahead. In FY24, revenue had increased by 8.7%. “The dilemma about prioritizing growth versus maintaining margins will persist, and to accelerate growth, margins may contract," points out Motilal Oswal Financial Services. FY25 will be a testing period for Colgate in terms of margin trajectory and volume expansion, added the brokerage.

Against this backdrop, the pricey valuation of Colgate stock is not comforting. After having risen by nearly 66% in the past one year, based on Bloomberg consensus estimates, the stock trades at almost 57 times estimated earnings for FY26.