Markets

Markets

ICICI Bank is going strong, but proposed LCR norms pose risk for sector

")

Summary

- ICICI Bank’s Q1FY25 performance continues to be a notch above the other large private banks on most parameters.

MUMBAI :

ICICI Bank’s core operating profit grew by 11% year-on-year in the June quarter (Q1FY25) to ₹15,412 crore. But it should be noted that a good part of this growth was aided by almost tripling of the dividend income from group companies to ₹894 crore. Excluding dividend income, core operating profit increased by 7%.

The bank is valued on a sum-of-the-parts (SoTP) basis, ascribing different values to the dividend paying group companies such as ICICI Securities. Thus, it is imperative to look at normalized earnings to avoid the risk of double counting. Sure, earnings in the case of price-to-earnings based valuation can also be normalized by deducting the dividend income from group companies. While consolidated financials solve the problem of double counting, it makes little sense in the case of ICICI Bank as some of its subsidiaries are engaged in diverse businesses such as insurance that have their unique accounting with revenue and costs.

Nevertheless, ICICI Bank’s Q1FY25 performance continues to be a notch above the other large private banks on most parameters. The annualized RoA of 2.36% is impressive, but what is more important is that it has been achieved by taking lower risk versus other banks. For instance, the high-risk portfolio comprising personal and credit card loans for ICICI Bank contributes 14% of the total loan portfolio as against 18% for Axis Bank. But ICICI Bank’s net interest margin (NIM) 4.36% is still higher than the latter at 4.05%.

Also Read: For DLF, luxury is the flavour of the season

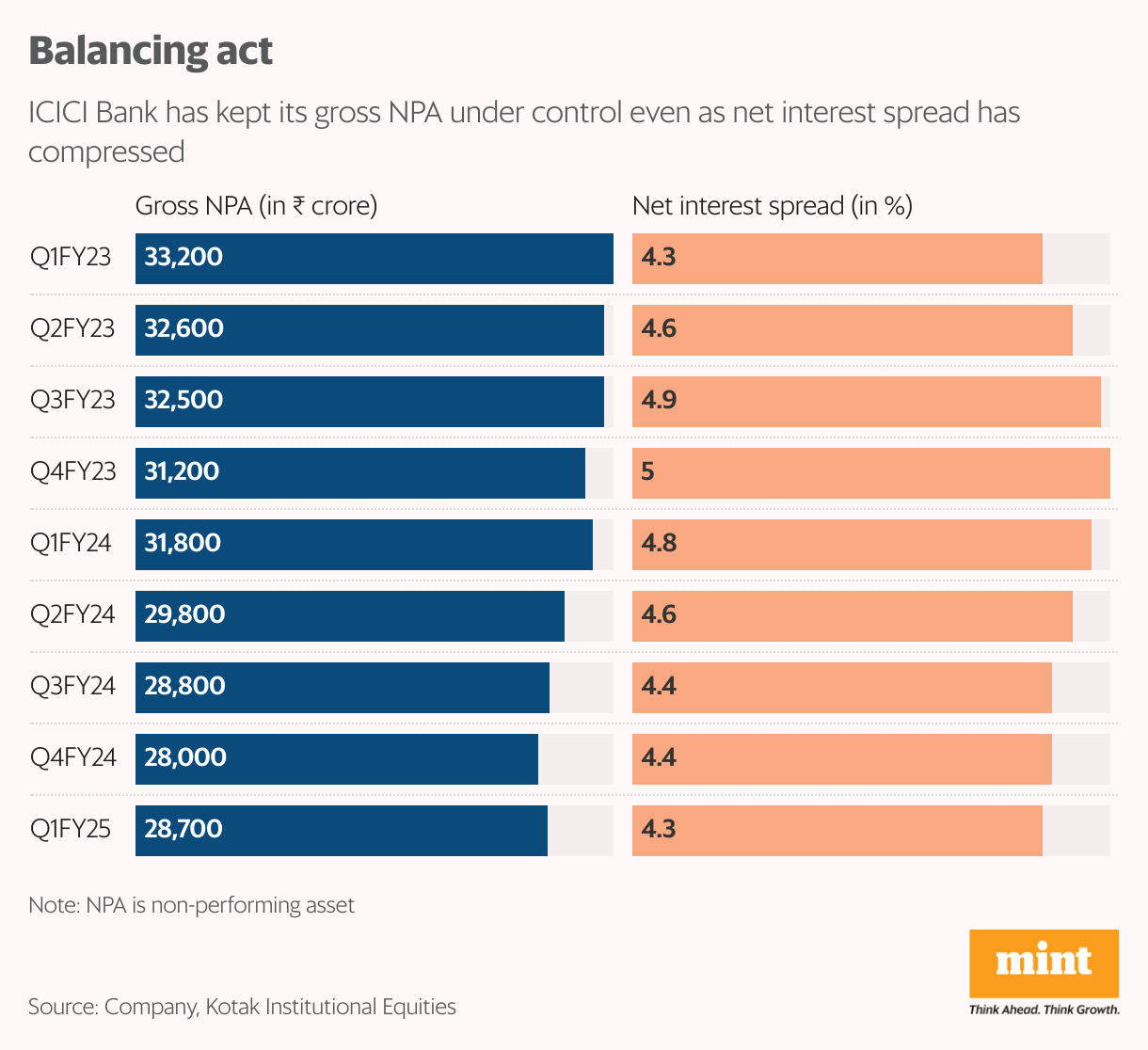

In Q1, ICICI Bank’s advances growth was 15.9% year-on-year. Importantly, the deposit growth rate is at a similar level, at a time when most banks are struggling to keep pace. The average low-cost funds in the form of CASA deposits grew by 9.7% year-on-year. The asset quality continues to be robust with gross NPA and net NPA remaining flat quarter-on-quarter at 2.15% and 0.43%, respectively. However, the outlook for credit cost is marginally higher as indicated by the management during the Q1 earnings call. This is because the pace of recoveries is likely to slow down, led by a shrinking pool of bad loans.

LCR hurdle

Meanwhile, the challenges for the banking sector are impacting ICICI Bank too. The pressure on lending rates, especially on corporate loans and mortgage loans, due to the competitive intensity is evident from the compression in the net interest spread. While cost of funds has been on the rise, there hasn’t been a corresponding increase in the lending rates.

According to Kotak Institutional Equities, ICICI Bank’s cost of funds increased to 5% in Q1FY25 from 4.2% in Q4FY23. Over this time, the yield on funds has increased by just 10 basis points to 9.3%. Thus, the net interest spread has been consistently narrowing to 4.3% in Q1FY25 from the peak of 5% from Q4FY23. One basis point is one hundredth of a percentage point.

Also Read: Margin headwinds loom for Nestlé India after unappetizing June quarter

In general, Reserve Bank of India’s recently released draft guidelines on liquidity coverage ratio (LCR) might make the going even tougher for banks. LCR means that a bank should have enough high-quality liquid assets including cash, government securities, etc. to meet potential withdrawals of 15% of wholesale deposits and 10% of retail deposits with an additional buffer for retail deposits mobilized through mobile and net banking. These norms could put further pressure on lenders with possible options for compliance being either higher deposit mobilization or reducing the lending by investing more in government securities. As of now, ICICI Bank refrained from giving any specific impact.

Kotak points out that ICICI Bank’s valuation premium compared to other private sector banks has expanded over the last five years. This could be owing to the bank’s superior return profile with RoA being consistently above 2% and strong provision buffers. For now, there is little to suggest a big threat to ICICI Bank’s premium valuation.

Also Read: Chart Beat: United Spirits' margin at multi-quarter high, but may not sustain