Markets

Markets

Execution challenges may weigh on L&T's growth prospects

Summary

- Profitability in Q1 was led by robust execution of international projects, while domestic ones remained subdued on account of labour shortages during the general elections.

- L&T is struggling to balance growth, working capital and margins, according to analysts at Ambit Capital.

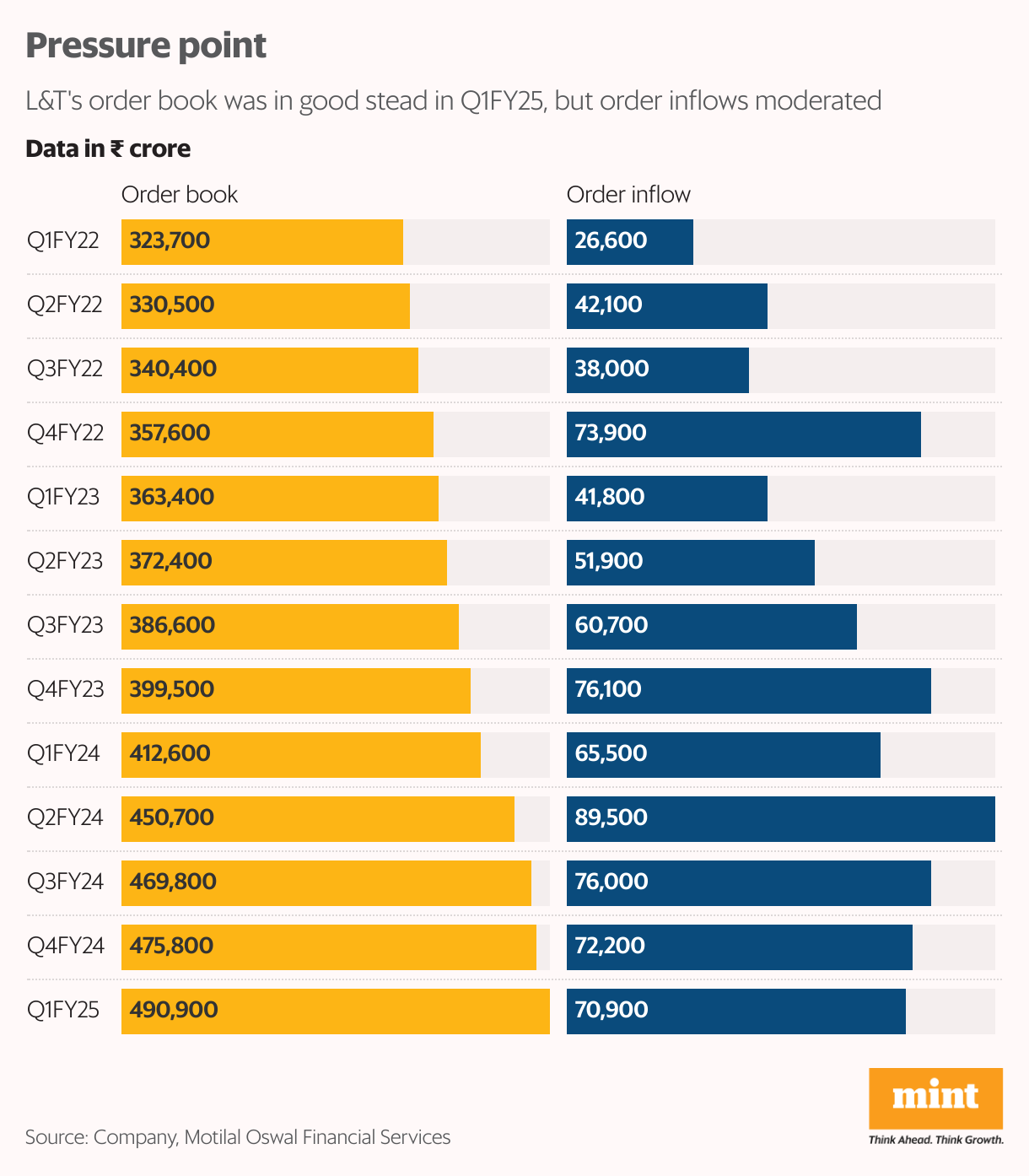

Larsen & Toubro Ltd’s stock shot up more than 2.5% on Thursday after its consolidated Ebitda increased 15% year-on-year to ₹5,615 crore in the June quarter (Q1FY25), slightly above Street estimates. Profitability was led by robust execution of international projects, while domestic ones remained subdued. The strong pipeline of orders worth ₹4.9 trillion – three times the trailing 12 months revenue of L&T’s core projects & manufacturing (P&M) business – should aid the growth momentum.

L&T has maintained the order inflow growth guidance of its P&M business at 10% year-on-year for FY25. In Q1FY25, P&M order inflow growth stood at 8%, backed by satisfactory growth in energy and hi-tech manufacturing.

Also read: Is Axis Bank's share price fall a knee-jerk reaction?

It’s worth noting here that the order prospects pipeline for the rest of this financial year has dropped to ₹9.07 trillion, which is 10% lower year-on-year. This is primarily due to a fall in the hydrocarbon prospects pipeline. The company was unable to secure some tenders, while other projects were deferred or shelved.

Against the backdrop, analysts at InCred Research Services said, “L&T is likely to miss its 10% order inflow growth guidance for FY25F mainly due to lower international order inflow." The broking firm lowered its profit-after-tax estimates by 2.3% for FY25 and 5.8% for FY26, mainly due to lower order inflows and revenue.

Elections caused labour shortage

The order backlog of ₹4.9 trillion was 20% higher than a year ago, with domestic orders accounting for ₹3 trillion and international orders ₹1.9 trillion. Execution in the domestic business during the quarter was affected by labour shortages on account of the general elections. A large chunk of L&T domestic order book comprises orders from the union government, state governments and public sector units.

With the elections out of the way, L&T expects domestic tendering activity to pick up. The pace of execution should also normalise in the second half of FY25. The government’s continued focus on capex the Budget is expected to buoy L&T’s domestic business as well.

Also read | HUL: Gradually improving outlook to test investors’ patience

The company aims to increase revenue by 15% in FY25. For its core business, L&T has maintained its operating margin guidance at 8.25%, similar to the FY24 level. In Q1FY25, the operating margin of the core business improved slightly to 7.6%. But the worry is that L&T has few levers to increase margins, so any improvement will be gradual.

A report by Nuvama Research said, “We are building in a core margin recovery to around 8.2% by FY26E given risks of (i) commodity cost hits and supply chain constraints, and (ii) slowdown in Middle East ordering as Saudi cuts/reallocates its capex plans."

Hyderabad metro and other issues

There are other lingering concerns, too, such as exposure to non-core assets of the Hyderabad Metro Project and Nabha Power Project. While L&T has been trying to divest the power project, it has not succeeded so far. Meanwhile, the Hyderabad metro continues to make losses. The lack of clarity when these assets will be monetised has dampened investor sentiment.

In its ‘Lakshya 2026’ plan, L&T had set a target of 18% return on equity versus the current 15%. One thing that could help L&T bridge this gap is reducing losses in the Hyderabad Metro Project. Core margins must also improve.

Also read: Oberoi Realty stock hinges on how it reinvests cash flows

The stock’s muted returns reflect the lack of excitement. So far this year, L&T stock is up just 3%, well below the Nifty50’s 13% gain. According to analysts at Ambit Capital, while the Street relishes order inflow growth, L&T is struggling to balance growth, working capital and margins. “Even as valuations suggest that the Street expects it to deliver on both parameters, a miss on any one will result in weak cash generation," it said in a report on 25 July.